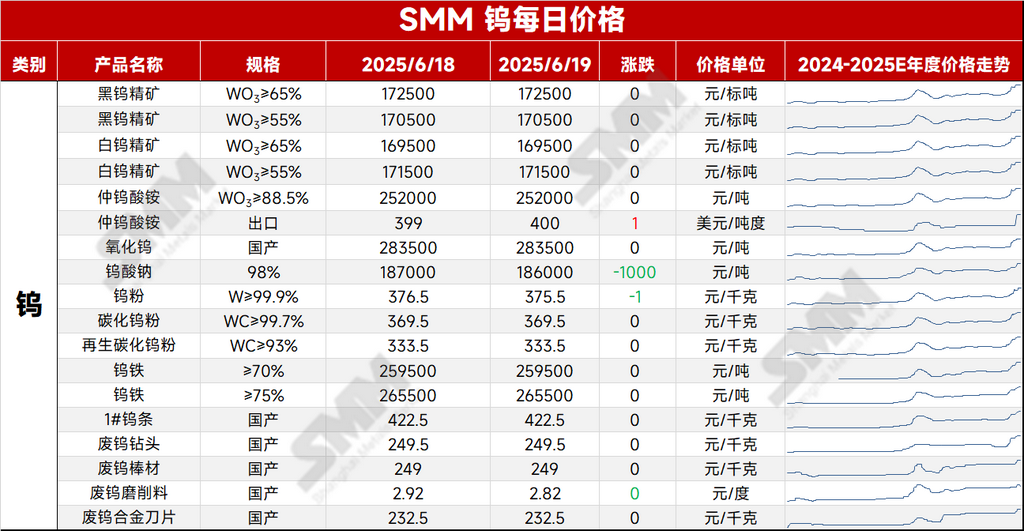

On June 19, the domestic tungsten market remained stable, with upstream suppliers mostly shipping under long-term contracts. Downstream smelters and cemented carbide enterprises saw weakened operations, primarily replenishing raw materials as needed. The overseas tungsten market continued to face tight supply, with prices rising slightly.

Ore segment: As of June 19, SMM's tungsten concentrate (65%) closed at 172,000-173,000 yuan/mtu, unchanged from the previous trading day. There were no reports of increased production in the ore segment, and market inventory levels remained low, limiting the potential for significant price adjustments.

Ammonium paratungstate (APT): Today, SMM's APT (≥88.5%) was quoted at 250,000-254,000 yuan/mt, with an average price of 252,000 yuan/mt, unchanged from the previous trading day. Affected by some suppliers' cashing in on arbitrage opportunities, market liquidity improved. However, with weakened orders from downstream enterprises, the market faced pressure, and prices showed a slight decline. Nevertheless, given the current poor industry profitability, cost support from enterprises remained strong. Overseas: On June 18, European ferrotungsten was priced at 51.7-52 US dollars/kg of tungsten (equivalent to 260,000-262,000 yuan/mtu in RMB), up 0.175 US dollars/kg of tungsten WoW. European APT was priced at 410-450 US dollars/mtu (equivalent to 261,000-286,000 yuan/mt in RMB).

In the short term, on the macro front, the US Fed maintained interest rates as expected. Fed Chairman Powell stated at a press conference that price increases triggered by tariffs would become more pronounced in the coming months, and the Fed needed to be confident that inflation was declining before initiating interest rate cuts. Additionally, the escalation of the Israel-Iran conflict and geopolitical instability have strengthened expectations for increased demand in overseas military industries. On the fundamentals side, the domestic tungsten market presents a tight balance between upstream and downstream sectors. While exports of intermediate tungsten products have declined, export demand for terminal products has improved. The market is undergoing a restructuring of the industry chain. Currently, ore supply and prices remain the dominant factors influencing the industry chain's pricing, with prices expected to remain high and consolidate in the short term. Subsequent focus should be on the new round of long-term contract procurement prices for tungsten enterprises.

[Quotation Status]

》View SMM's tungsten and molybdenum product quotations, data, and market analysis

》Click to view SMM's molybdenum spot quotations

》Subscribe to view historical price trends of SMM's metal spot products